What I did to secure my credit information

I don’t like debt. However, like most people, I use debt – a mortgage, a loan for solar, credit cards, student loans (2021 update – no more student loans!), a car loan (2024 update – no more car loans!). Although I dislike it, debt is valuable. Loans have helped me obtain a career I enjoy, live in a comfortable home, and make a great life for my family. In the future I will likely apply for more loans, which means lenders will look at my credit record. So, I have to pay attention to my “credit worthiness,” as the gatekeeper to debt. This post is about what I did to help secure my credit in response to the massive loss of personal data through Equifax (143 million people’s personal data may have been lost!!). But first, a rant against the powerful.

Rant against the powerful and powerfully irresponsible

Equifax, as a credit rating agency, is powerful. I don’t have a problem with power, but as SpiderMan timelessly said,

“With great power comes great responsibility.”

The leaders of Equifax are showing a reprehensible lack of responsibility. Here are a few ways they hold power over me:

1) Somehow, they have the right to collect all of my personal information without my explicit consent (ok, I probably gave consent by clicking “yes” to all of those tiny little “I agree to terms and service” buttons, but does that really count??).

2) They somehow crunch that data into a “credit score” that affects how other agencies trust me, by affecting my ability to access debt.

3) They also leverage my personal data to provide online identity checks.

4) Other ways that I haven’t thought of…

With great power SHOULD come great responsibility. But what did Equifax do with their power?

1) Equifax executives withheld the mistake from the public. They allegedly knew of the data breach months before announcing it publicly.

2) Equifax executives appeared to profit from their knowledge. They allegedly sold stock after the data breach was discovered, but before it was announced publicly.

3) Equifax, the company, tried to offer a “fix” by forcing customers to give up their right to join a class action lawsuit against the company (they have since rescinded this “fix”).

4) Equifax, the company, is STILL is advertising mediocre band-aid fixes on their website, while the more robust “Credit/security freeze” option is hidden. Most of these options are subscription-based “services.” So, to summarize: Equifax collects my personal information. Then, they offer to sell me a service so that 3rd parties can’t access my information. WTF??!! This sounds like extortion!

Equifax is showing no sense of responsibility. I wish Spider Man could swoop in and spin a web of justice around the irresponsible executives. Confiscate their second homes! Sell their fancy cars!! Gut their stock option accounts!!! Donate the proceeds to some sort of non-profit that helps people build their personal credit!!!!

Rant done. Here is why I decided to do something

Data breaches have happened before. In the past, I have grimaced, but filed the story in “too hard to understand or control” section of my mental filing system. Those files never get dealt with. But then, my sister sent me a text saying that she was “freezing her credit.” My sister? She is a firebrand and an activist, but usually only on matters like social justice or a new banana bread recipe. So when I saw her send out a call to action in response to this whole data breach from Equifax, I figured I should do something as well. The problem I had was, what to do?

I hate doing things without some knowledge and research to back up my actions. Sometimes my position leads me to “paralysis of analysis,” especially when there are too many options. I began doing some research. Luckily, in this case, it seemed my options were limited to:

1) I could freeze my credit (like my sister did), where my credit report is blocked from viewing by anyone, until I agree to unfreeze it.

2) I could initiate a “credit fraud alert service” where I would be notified whenever someone tried to apply for credit.

3) I could choose whatever solution is being offered by Equifax (no chance I would select this option, as I have less-than-zero trust for this company)

4) I could do nothing

Eventually, I decided to freeze my credit with each different agency. A credit freeze prevents anyone from accessing my credit information. In order to allow someone to access my credit history, I must unfreeze it. The downside to a credit freeze is that I will need to unfreeze my credit if I need to access it in the future. But, putting the cookie jar on a higher shelf is probably a good way to manage my own behavior. Kind of like when my wife and I had to replace our hot water heater. We considered an on-demand unit with unlimited hot water. But, then we thought about our kids soon becoming teenagers, and how long they might wish to sit under an endless stream of hot water. We opted for the 50-gallon model. Our hot water runs out.

I discovered that managing my credits freezing and unfreezing may be a bit easier than I thought initially, and less expensive. I read an excellent blogpost by Michael Toub, called “Which Protects You Better: a Credit Freeze or Credit Monitoring?” He froze his credit, but realized that if you ask a potential lender which agency they contact, you can selectively unfreeze your credit and re-freeze after the request has been pushed through. Toub reported that one year he switched cell phone carriers, applied for a new credit card, and leased a car. He was able to selectively unfreeze and re-freeze his credit for under $30. (2024 update. This blog post may no longer be available. However, Nerd Wallet has a pretty decent discussion of credit freezes vs. credit monitoring. See the bottom of this page for the URL.

A credit monitoring service is easier, and less expensive, to implement. Supposedly, you can sign up with one agency, say TransUnion, and the service request reaches out to all three. It is a free service (though it will probably be an invitation to offer you other not-so-free services). You would get a quick alert when your credit report was accessed. Thus, if someone tried to open up a new credit card in your name, you would be notified. If that someone was not you, you could…. take action to block it? I guess that is how it would work. The big downside to this service is that it only lasts 90 days. I would have to renew it every 90 days. I know myself, and know that I would never remember to renew it. I’d shift back to “forget or ignore” mode almost immediately. I barely remember to put out my recycling every week, and that problem is in my face (and my nose) when I forget!

Here is how I did it

1) First, I checked my credit score. To be honest, this was an accidental step, because my bank had a “Check your FICO score button.” I clicked on it, and voila, my credit score! Cool, thanks Whatcom Educational Credit Union, www.wecu.com! I like my local, community bank. I pay them piles of dollars every month for interest on our home loan. I still love them. That is what trust and service can do Equifax scumballs! Oops, sorry, my rant was supposed to be over. If my bank hadn’t offered it for free, I would not have checked the score.

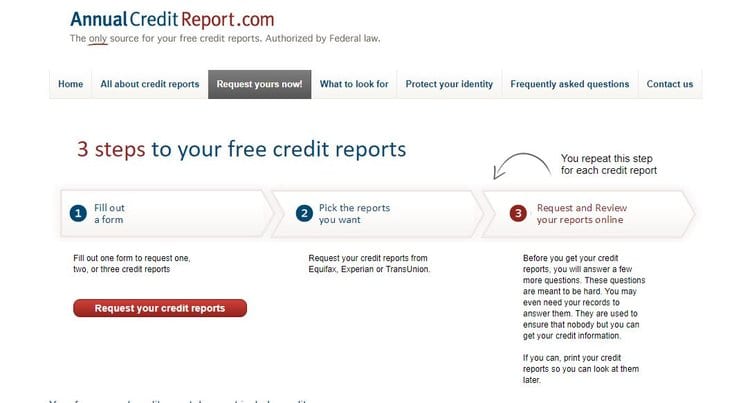

2) Next, I went to Annual Credit Report.com. It took me about 45 minutes to get each of my credit reports and to review them. I knew I was supposed to do this annually, so I guess I can be thankful to Equifax for spurring me to act??

SCREEN SHOT TO GET FREE COPIES OF YOUR CREDIT REPORT

Next, I froze my credit through the three big credit ratings agencies. I contacted each agency online, froze my credit, received a PIN, and typed the PIN into my online password storage app. Then, I made myself another cup of coffee, and returned to my regular life. This process took me about 30 minutes in total, and cost me $11. (2023 update: I’ve heard that the credit reporting agencies no longer charge for this service).

3) I froze my credit through Experian. This process was somewhat easy. I went to their home page, which offers lots of expensive plans and ways to monitor your credit. After a little digging, I found the “Security Freeze option” listed on the Support tab. I selected the option “Add a security freeze.” It cost me a one-time fee of $11.01 (cost will vary by state). (2023 update: I’ve heard that the credit reporting agencies no longer charge for this service). The direct link to this page is: https://www.experian.com/freeze/center.html.

SCREEN SHOT OF EXPERIAN’S “SECURITY FREEZE” PAGE.

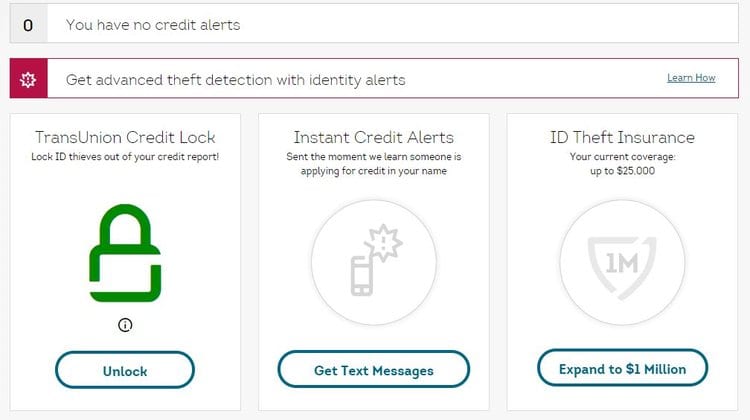

4) I signed up for TransUnion’s “True Identity” free service. This service allowed me to “lock” and “unlock” my credit at will. I haven’t tested to see if it actually works, but I am intrigued. This service seems like a very consumer-friendly option, and one that actually improves my trust with TransUnion. They collect my information, but give ME an option of controlling who and when the who can view it. WOW! WHAT A CONCEPT! Slimy greedy bastards at Equifax should take some notes.

Here is the link to TransUnion’s freezing your credit site

https://www.transunion.com/credit-freeze

I clicked on “My Free Identity Protection.” I have not yet decided if I also need to put a separate “credit freeze” on. Here is what the screen looks like after I locked my credit:

SCREEN SHOT AFTER I “LOCKED MY CREDIT” THROUGH TRANSUNION’S TRUE IDENTITY PROGRAM

5) Finally, I went to the dreaded Equifax website. I looked around for the “I hate you and never collect any of my personal information” button. That button does not exist. Then, I looked for the “Credit Freeze button.” That option also did not appear to exist. Instead, here is what they offer as “products and solutions.” I am particularly incensed by the “Best Value for Families” option, $30/month to not allow Equifax to share your personal information that they collected from you??!! In 2017, here were the options presented:

SCREEN SHOT FROM EQUIFAX “PRODUCTS AND SOLUTIONS” PAGE

Frustrated, I re-read the blog post by Michael Toub, and found had the link to a Credit Security Freeze through Equifax. Here is the direct link:

How to freeze credit with Equifax

Strangely, the credit lock through Equifax did not seem to cost anything.

End Notes

If you want more information, I highly encourage you to read these two blogposts I used for reference:

“Credit Lock vs. Freeze: How They Compare and When to Use Them” Nerd Wallet. Authors: Lauren Schwahn and Amrita Jayakumar. https://www.nerdwallet.com/article/finance/credit-lock-and-credit-freeze

Brian Krebs, “The Equifax Breach: What you should know.” https://krebsonsecurity.com/2017/09/the-equifax-breach-what-you-should-know/. I found Krebs blogpost because Michael Kitces referred it from his excellent “Nerd’s Eye View” and weekend reading for financial advisors blogpost. I have a LOT of trust in what Kitces puts out.

Michael Toub, “Which Protects You Better: a Credit Freeze or Credit Monitoring?” http://www.doughroller.net/credit/security-freeze-vs-credit-monitoring/. This blogpost offers lots really good information. There is also lots of advertising, which is probably how the blogger makes money, so just be careful of what you click of from the website.

I hope this helps you. Full disclosure: My name is John Chesbrough. I neither receive nor earn any compensation from this blogpost. However, I DO earn compensation as a financial planner and investment adviser working directly with, and for, my clients. I take security and people’s lives seriously. I do not practice in extortion, but I DO wear my fiduciary badge with pride. If you would like more information about working with a fiduciary financial planner, please contact me here.