Talking about investing with my kids

It is investment management report writing season for me, so this week I am going to write about investing. Investing and asset management is only one piece of financial planning, but it is a crucial one. Many of our long-term goals rely on the power of delayed gratification. We delay spending money now to invest, in the hopes that it will be worth more in the future. This post is about investing in stocks. But, my real message is trying to teach young people about delayed gratification. In addition, I think this story gives some insight into how I think about investing in individual businesses. This investment style is not for everyone, and I don’t advocate it for all of my clients. But, that’s enough preamble. To the story of how I talked stocks with three teenagers for over an hour straight, and how they ignored their phones for the entire time to engage with this geeky adult (me).

Last week, I was driving home from the Seattle airport with my 11-year old son Poe, 13-year old daughter Mia, and their 17-year-old cousin Lane. We were somber; we had just returned from a week in Mexican waves and sun. As we merged onto the freeway, my nephew started plugging earphones in, Mia turned on her phone, and Porter asked for the iPad. I started listening to a podcast. But then I realized that after a week together, we were about to separate. I wanted to stay engaged with each other for the last hour. So, I tried to spark a conversation about investing in stocks.

“Ooohhh, investing in stocks,” you might be thinking, your brain waves rippling with sarcasm. Yawn. (My wife was also in the car. The quote/action are hers).

I’ll admit, I felt a little desperate, like a nerdy teacher drolling on about the Conservation of Energy, a seemingly insignificant bit of noise to an adolescent world. Well, I am a nerdy teacher, so I was in familiar territory. Fortunately, I had a hook – the kids have some money.

A few years ago, my father-in-law and I opened Coverdell Educational Savings Accounts for each grandkid. The goal was to use the accounts as a way to get the kids to think about, and “buy in” to their own financial futures, and also be an additional source of funding for college. Every year or so, I have a chat with each kid, and ask them about companies they observe. I ask them to do a little thinking, and to choose one or two companies to invest in. We do a little research together, and I make sure they are buying quality businesses. I have them write down their thoughts. They choose, and we buy a few shares. In several years, I intend to let them know how their investments have done. Mostly, I hope they experience delayed gratification. In addition, I want them to experience investing the way many successful investors (like Warren Buffet) do: buy shares in high-quality businesses, and hold onto those shares for a long time. Our research is by no means thorough, and these are not big dollar accounts. Gains or losses in share price won’t affect whether or not they can to college.

I told the kids that I needed to buy stock for each of them. To my utter delight, all three kids got way into our conversation. The earbuds came out. Mia shut her phone and picked up a pencil. Porter never touched the iPad. Lane used his phone, but only (mostly) for research. I am not sure it would be an easy discussion for most people to facilitate with their kids. But, I am blogging about our conversation because I think it illustrates the first level of my own thinking about investments. It also illustrates how thoughtful and tuned in kids really are to their surroundings.

Quality businesses – the research

The first question I posed to the kids was,

What are some companies you are aware of that are getting more and more popular?

Lane immediately replied, “Amazon.” The other two agreed. Porter asked about Youtube, so I told him it was owned by Google. Google went on the list. Mia added Starbucks. Toyota, Facebook, and Netflix were included. Lane found out that Disney was buying the rights to 21st Century Fox. We added Disney. That led to my next question:

How does each company make money?

I told them about Disney – theme parks, ESPN, and movie studios (including Pixar, Star Wars AND Marvel!!). They were shocked. Next, I asked about Google. Lane knew the answer, “advertising.” I agreed. But Porter asked, “what do you mean, advertising?”

Lane responded, “You know those ads at the beginning of every Youtube video you watch?” Porter got quiet for a moment, then the curtain was lifted.

Whoa, he whispered, followed by an out-loud, “Whoa,” followed by a proclamation: “WHOA!” It was as if he just noticed the Earth was round. I could literally see his thinking:

“Whoa”, (oh, like those ads).

“Whoa” (like, every Youtube video I’ve watched has an ad).

“WHOA!” (like, oh my god, that video with 2.7 million likes had an ad attached 2.7 million times!). Hysterical.

Amazon, Starbucks and Toyota’s business models were easier to understand, and a bit less mind-blowing.

Next, I extended the original question. Do you think the companies you are talking about will get more and more popular over time?

This was a little bit tougher to answer. They all thought Amazon, for sure. Disney, yes. Google, probably. Mia wondered out loud about Starbucks. She realized that was a difficult question to answer (and that she would need facts before proceeding further. Yay for research!). Porter brought up advertisements by Toyota during the Olympics where they were positioning the company to be about “movement” rather than just cars. Interesting.

Next question. Could the companies be easily replaced by another company?

We went through them one by one. Amazon earned a tepid “yes, but hard,” Google was a yes. Disney a definite “No.” We venture into a discussion about Netflix, and how they were once a DVD-by-mail company, and very replaceable. Next they started streaming movies over the internet. Still replaceable. Lane grabbed the bait, “And now they make tons of their own shows.” Yes!

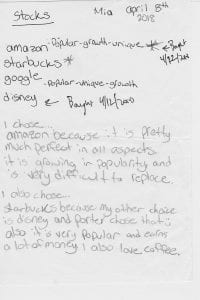

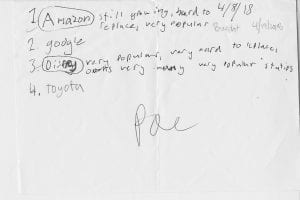

I made them rank the companies from hardest to replace to easiest. In my opinion, this question is one of the key tenets of investing. There are lots of good ideas and trends out there. But, if a company is easily replaceable, its economic strength will quickly be eaten away by competition. Warren Buffet calls this idea a company’s “moat.” It can lead to pricing power, where a company can raise prices over time with their customers remain customers. Sometimes pricing power comes on the back of love (Starbucks or Costco?), sometimes by force/coersion (Comcast?). Mia, Poe and Lane agreed that Disney was the hardest to replace, while Toyota and 21st century fox were probably the easiest. Savvy thinkers about business!

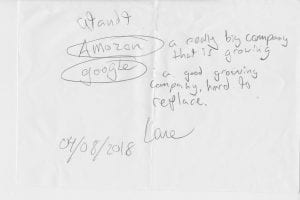

Wrap up. Now, I informed them: “you must choose two, and write down your reasons.” I collected their responses, and will keep them in a notebook. Here are their notes:

Buy and hold

Once we had done the “research,” I bought some shares for each kid. I don’t plan to say too much about it to them for years. My hope is that five or ten years from now (a bit sooner for my nephew), we will look at their accounts, and they will see growth in the value of their investments. Or course, there is risk in investing. Their investments may lose money. But, that would be a valuable lesson as well.

The time period of ownership is incredibly important. In the short-term, stocks move in a “herky-jerky” fashion (that is the technical name of it). Academic research suggests short-term movement is very difficult to predict, because much of it is based on sentiment. In the long-run however, a company’s stock price will be based on its underlying economic value. Again, I turn to the oracle of investing, Warren Buffet, who famously said, “In the short term the stock market is a voting machine, in the long term a weighing machine.” My style of investing relies on a long-term frame of mind.

My own investment research process starts with the same questions as I posed to the kids. I am a business-focused investor. However, there are a few more layers before I make a “buy” decision. I dive into the numbers. I read the company reports. I research the quality of management. I create a “value range” for what I think the company should be worth (based on what the company has, and what it makes). I compare the current stock price to the value of the business. I read thoughts from other investment professionals (notably content produced by the Motley Fool).

This type of investment style is called “Fundamental analysis.” I think it is fun. Most people think I am mental. But, it has some nice outcomes – like a growing investment portfolio to fund things that are important to me and my family (college, travel, early retirement).

Full disclosure and caution about investing

My clients and I may (and do) own shares of all companies mentioned here (except Toyota). Investing in stocks is inherently risky. There is no guarantee that the value of an investment will grow over time. In fact, an investment may lose all of its value over time. Risk and return. Return and risk. You can’t have one without the other. It’s sort of like “There’s no such thing as a free lunch.” I once had a Biology professor say that this saying (about lunch) was just an off-hand summary of the Law of Conservation of Energy. That’s another important lesson, maybe for another day and another blogpost. Thanks for reading!