Investing 103: What investments should you choose?

My father-in-law recently found a buried treasure. Deep in the back of a filing cabinet, he discovered a forgotten envelope containing several US savings bonds.

Fun! Unexpected money! The bonds were made of real paper; they had a good feel – squared corners, colorful bold print. They were just as sturdy and crisp as the day he bought them 30 years ago. The printed, or “face value” was $500. He had bought the bonds for $250 (that’s how series EE savings bonds work) to help his daughter pay for college, and because Boeing employees at that time were encouraged to by Savings bonds. But, he forgot about them. I am guessing that paying for college didn’t have the same financial pressure then as it does today.

Thirty years later, after I was fortunate enough to meet and marry his daughter, he delivered them to her. She redeemed them, and was pleasantly surprised by an $850 value. His investment of $250 had turned into about $850 over 30 years. That’s pretty good, the money had more than tripled.

But here is the thing: over 30 years, prices have gone up. In 1990, gas cost about $1/gallon, and a movie ticket was about $4.22.

Image courtesy of Blakey Auto Plex. [1]

Image courtesy of Twentieth Century Fox [2]

Today, movies and gas are about 3 or 4 times as expensive as they were in 1990. So while the savings bond investment tripled over 30 years, so did prices. Thus, the savings bond basically just kept up with inflation. Just for comparison, if that same investment of $250 had been put into a S&P 500 index fund in 1990, and dividends were reinvested over time, it would have been worth $3,700 now. That would have been an increase of 14 times the original value. When my father-in-law originally bought the bonds, he intended them to be used for my wife’s college costs, which were only a few years away. So, I don’t fault his investment choice. He selected an investment that matched his time-frame. But, then he forgot about them, and the investment unintentionally turned into a long-term time frame. The investment no longer matched the time-frame.

This blog is the third in my mini-series about creating an investment process. The reason I am doing so is in response to a question, or worry, that I keep hearing:

“Isn’t it a bad time to get into the stock market right now?” or “It seems as if a single Tweet could blow my investments up…” or “Whenever I’ve put money into the market, the market crashes the next month. It’s like I have some sort of bad financial kharma that I am re-paying.”

The reality is, most people need investments in order to fund our future goals. But, it is important to put purpose behind your investment decisions. This post is a continuation of a story about Ava and Raj, and the Investment Policy Statement they developed to put purpose and a plan behind their investment process. The other posts in this series are:

Investing 101 – Why invest? Create a process and a plan (previous post)

Investing 103 – What? What should you invest in? (this blog post)

Investing 201 – What if? Investment Returns and Risk

Investing 202 – Diversification and fees. Why do they matter? (future blog post)

Investing 301 – How? Create a comprehensive investing strategy. (future blog post)

First you need an investment account

Before you choose an appropriate investment, you need an appropriate account to hold it. It’s as if you want a garden at your home. Before going to the store to buy some starts, you might want to know where you are going to plant them. If you live in an apartment or condo, without much space, it wouldn’t make much sense to buy an apple tree. If you have some yard, you might want to consider how much space to devote to vegetables and fruits vs. perennials to provide color and greenery year-round.

This post is focused on types of investments (or plants), rather than types of accounts (or what land/planters you will use to house your plants). To read more about types of investment accounts, you can read these two previous posts I wrote:

Save for Retirement part 2 – What type of account should I use? I discussion of different investment accounts.

Save for Retirement part 3 – Why a tax-diversified strategy makes good sense. How using different tax-advantaged accounts can help you long-term retirement goals.

Types of investments

If you start shopping around, you will realize that there is an bewildering array of investment products out there: mutual funds with A shares or B shares, Exchange Traded Funds (ETFs), whole life insurance, annuities, gold/silver, bonds, CDs, money market accounts, hedge funds, alternative investment funds, etc.

It’s like going to a plant nursery, but the nursery doesn’t have any real plants for you to look at. It is just a giant book, with lists of plants by name. There aren’t even any pictures. What the book does have, is a bunch of numbers and graphs about plant height, shade requirements, and average fruit yield. Only a die-hard gardener could really use such a book to effectively plant their garden.

But, that is what you are asked to do with investments. Despite the ominous thickness of the catalog, most products are just re-packaging of a few classes of investments stocks, bonds, real estate, or “alternatives.”

Stocks are pieces of ownership of a company. When you own a single share of a company, say Apple, you are an owner of a sliver of that company. Technically, you own a right to a slice of the future profits of that company. In the case of Apple, one share is, as of this writing, worth a 0.00000002% slice of Apple’s future profits. Get it, an apple slice? Ha!

You may be surprised to learn that the little 0.00000002% of Apple’s profit was close to $10 last year. Or perhaps this is unsurprising to you, as you notice what people are staring for an average of 2-3 hours per day. In the garden analogy, stocks are like little plant starts. They stand a decent chance to grow quickly, but there are many risks. And there are lots of types of plants. Over time, a fresh little start in your garden can turn into a fixture – a thick stemmed grape vine that shades your awning and delivers fruit year after year. But, it is also true that plants can wither, often unexpectedly.

Bonds are little loans that you (the investor) own. You might have loaned your money to a company (like Apple), or to a government. As an investor, you are promised to be paid back your original investment plus interest. Bonds are generally safer investments than stocks for several reasons. For one, bondholders have a legal right to be paid back before stock owners. Secondly, future returns are more predictable. In the garden analogy, a bond is a bit like a fully-grown, potted plant. Maybe it’s a cherry tomato plant. The nursery has already raised it from youth, so you know how much space it will take in your garden, plus you know how many little toms you’ll get to munch.

Real estate is ownership of real property – a house or a piece of land. I don’t think an analogy is needed here. Owning real estate is like owning a garden. Direct ownership has the benefit of “you can kick the tires,” but it also means the buyer must be aware of the product, and must deal with ongoing maintenance costs and efforts.

Alternative investments is a broader class of anything else that may hold, or appreciate value over time – Art, gold, silver, season tickets to the Seahawks, the Seattle Sonics franchise (grrr…).

But, what about the thick catalog of investment offerings?

Most people don’t own individual stocks or bonds. Most people own collections of investments through mutual funds or Exchange Traded Funds (ETFs). These products are just collections of individual stocks or bonds. They are like the seed packets that bundle lots of types of plants – like “Wild flowers.” You basically know what is inside (wild flowers) but, are they lupin? shooting star? petunias? How many of each type?

Most of the products in the catalog of investment options are just re-packaged groups of stocks or bonds. In fact, most of the investments you own through your retirement plan or your college savings account are likely re-packaged stocks and/or bonds. In further fact, most financial products, from life insurance to a pension to a Guaranteed Tuition Plan are based on the ownership of stocks and bonds.

How should you choose an appropriate investment?

Before investing, you should always consider big picture needs for your money: paying off high-interest debt and saving for an emergency fund are generally considered a better use of your funds. Once those are taken care of, you should build and investment strategy. Specifically, you should ask,

What do you need your money for? How much will you need? If it turns out you already have enough money to pay for everything in your future, “don’t invest” is a pretty good option. If you only need a modest return, the stability of bond returns may be acceptable. Why subject your money to more risk than you need to? For many people though, their long-term goals will require a greater pot of money than a hole in the back yard or savings bonds will provide.

The next question is, “When will you need your money?” (the time-frame). I wrote about time-frames in the previous post (click here to read it). However, we are now veering into territory where individual circumstances, and emotional temperament matters tremendously. Thus, my discussion should probably have an asterisk behind every sentence that says something like “This information applies to a generalized Jane Doe. I’ve never met Jane. You not Jane. So, this information is not meant to be a substitute for individualized advice.”*

Long-term money

For your long-term money that you need to grow, you should probably own a healthy dose of stocks and/or real estate. The exact amount will depend on your risk tolerance, age, need, etc. Stocks are the most common investment for long-term money that needs to grow. Real estate is also used. It is useful to explore why each is appropriate (The whole knowledge is power thing), but I will reserve that discussion to my next post about return and risk.

Short-term money

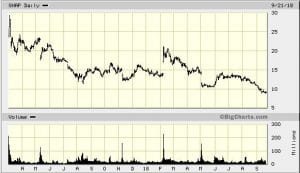

The reason to not put short-term money into stocks is because, the stock price is based on future profits. But, the future is inherently unknown. If expectations of future profits become brighter, then the stock price generally rises. But, if expectations of future profits fall, then the stock price generally falls. Because stock prices are based on a fundamentally unknown space (the future), they tend to shift around, sometimes a lot. This is called risk. It would be a real bummer if you invested $1,000 of your daughter’s college education fund that she needed 2 years from now into a “hot technology stock” that lost 50% of its value within six months. Snapchat is a very popular app right now, that a college-bound daughter may use. One year ago, Snapchat the stock, was a “hot topic” in financial media. Behold the share price of “SNAP” over the last year:

Real estate is also not a great short-term investment, but mostly because it is expensive to invest in, and difficult to extract your money. Real estate has low liquidity.

Bonds and fixed income ARE a good place to park short-term money. The reason TO put short-term into some sort of bond fund, is because of the predictability. In the Fall of 2018, I can find a 2-year bond that pays around a 3% interest rate. A $1,000 investment today would become $1,060 two years from now. That’s not too exciting, but you should be nodding your head and saying “exactly!” The point is to not be too exciting for money that you will need within two years.

Some historical examples

Let’s look at a couple historical examples with the $250 investment I started out this post with.

Bonds. As I stated before, the investment grew to $850 through US savings bonds. It matched inflation.

Stock. If my father-in-law invested the $250 in Apple stock 30 years ago, it would be worth $28,000 today. But, choosing Apple is cherry picking. (Ha, more fruit puns!) Thirty years ago there was no hint of the iPod or iPhone. He also could have invested in another fast growing company at the time, Blockbuster. In that case, the $250 investment would have gone to zero due to Blockbuster’s bankruptcy. I expect he would have felt pretty bad about lighting his daughter’s money on fire. Of course, if he’d invested $125 in each, his investment would have grown to $14,000. Hey, that’s the beginning of diversification. I will dive into that topic in part 5 of this series. Blatant foreshadowing.

The stock market. A simpler decision than “which stock?” would be to just buy a little slice of all US stocks. The Standards & Poor 500 (S&P500) is such a basket – 500 of the largest US publicly traded companies. By “owning the index,” an investor owns a bit (bite?) of Apple, and they used to own an evaporating position in Blockbuster. But, by using the fancy idea of “don’t put all your eggs in one basket,” the $250 would have turned into about $3,800 today (if dividends were re-invested).

Real estate. What if somehow the $250 was invested the Seattle real estate market? Of course, it would be nearly impossible to do so with such a small number, but I can still do the math. Back in the early 1990s, the median home price in King County was between $130,000 to $140,000. In Fall 2018, it is around $700,000. If he could have invested directly in the real estate market, his $250 would have turned into close to $1,300. Better than bonds, but not that much better (however, this ignore the effect of leverage which I will return to in part 4 of this series).

A return to Ava and Raj

In my previous two posts about building an investment process, I introduced Ava and Raj. They are a married couple in their early 50s, whose kids are now in college. They have a sound current financial situation, and are focused on an effective Investment Process for their investments. They have created goals, and organized their current resources:

Their goals:

- Maintain a $30,000 emergency fund. (short-term time frame)

- Help their daughter Abby pay for her schooling. They will pay for this through their Dream Ahead 529 plan, current cash flows, some loans, and an expectation that Abby works. (short-term time frame)

- Fund Ava going self-employed as a nurse practitioner. (short-term time frame)

- Save for a vacation home. They want to have around $100,000 for a down-payment in 10 years. (long-term, shifting to intermediate-term time frame as the purchase gets closer)

- Retire at normal retirement age of 65. They expect to need about $1.8 million. (long-term time frame)

Their resources:

- $50,000 in savings. They will use it for emergency fund, and as seed money for Ava’s business. Short-term.

- Ava has a 401k with about $600,000 in it. Long-term.

- Raj has a 403b plan with $250,000. Long-term.

Their cash flows:

- They will save for the down-payment on a vacation house by opening Roth IRA accounts, and fully fund them ($6,500 per year each). Long, then intermediate term.

- They will save excess cash flows into Ava’s 401k. Long-term.

Their investment choices:

- Short-term money. Their bank account, and money for the next 4 years of Abby’s school expenses will be deposited into a “high-yield” online bank account like Ally bank. They expect to earn only around 1-2% in interest, but the money will be safe, and ready to use.

- Intermediate-term money. For the first five years, they will invest the money in passively managed, broadly diversified indexes of stocks (a mix of US and international). Once they are five years from needing their money, they will invest all new funds into short-duration bonds, AND reduce their stock exposure in their existing portfolio by 20% until it is 100% in bonds and cash by the time they need it.

- Long-term money. They determined that they need only a 4.5% return to amass $1.8 million by retirement. Because they can, they decide to shoot for a slightly higher return of 6%. To achieve such a return, they opt for an asset allocation of 60% stocks, and 40% bonds. Within those allocations, they will diversify across domestic and US based securities. For the math, see note [3].

Final thoughts

When my father-in-law invested his money in US savings bonds, he did so with an appropriate short-term time frame. He is a pretty savvy guy, so if he was considering a 30-year time-frame, he would have chosen a different investment choice. His mis-match between time-frame and investment was inadvertent. But, I meet many people who are nervous about the stock market. They don’t trust what they don’t understand. They often have a mis-match between what they need, and how they are invested. It is important to recognize risks, it is equally important to manage your finances to meet your future goals. This is one of the primary jobs of a good financial planner.

Well done! You’ve reached the end of this post. To read more in this series about creating an investment plan, you can read the following:

Investing 101 – Why invest? Have a process and a plan (previous post)

Investing 102 – When? Manage your emotions through time-frame and liquidity (previous post)

Investing 103 – What investments should you choose (this post)

Investing 201 – What If? Investment returns and risk

Investing 202 – Diversification and fees. Why do they matter? (future blog post)

Investing 301 – Create a comprehensive investing strategy. (future blog post)

Or, you may be interested in:

How we (John and Liz) take our fiduciary responsibilities seriously, and why we think fee-only is the right way to work with clients About Us.

Or, you can read more of John’s writings about finance matters that matter, on the main blog page on Trail Financial Planning

If you’d like to have further conversation about your own goals, resources, time-frames, or investment allocation, we offer free 30 minute consultations. Just go to our contact page, submit your digits and ask to speak to John or Liz.

*Whoa, you are reading the asterisks! You must like this stuff. Or, investing scares the hell out of you, so you try to learn as much as possible. If you would like to talk more, consider reaching out to talk. (See contact link in previous paragraph).

WOW, you are still reading! You win a gold star! If you are hungry for more information about finances, you can visit our main blog page here, to see more writings by John.

References

[1] – Source: Image URL no longer available

[2] – Source: https://247wallst.com/special-report/2017/08/11/cost-of-a-movie-ticket-the-year-you-were-born/7/

[3] – Ava and Raj “expect” stocks to achieve an 8% future return. They expect bonds to achieve a 3% future return. To reach an expected 6% overall goal, they select 60% stock/40% bonds. The math is as follows: (0.6 * 8%) + (0.4 *3%) = 6%.